*TeachersRetire is not affiliated with, endorsed or sponsored by PSERS*

Many PSERS retirees find that income taxes are one of up their largest expenses in retirement. The reason for this is simple- most of the income that a retired educator has is taxable. This includes the PSERS pension, Social Security, the 403(b) and IRAs. Due to this, it is common for a educator to find themselves in the same tax bracket in retirement as they were while working. What a bummer!

So, the big question is- what can a retiring Pennsylvania educator do to keep more of their money and pay less taxes once they stop working? We’re going to answer that question by exploring one strategy that might help you lower the amount of taxes you pay in retirement by taking advantage of the years when you are in a lower tax bracket.

As always, the information that’s presented in this article is not tax advice and you should consult a CPA or tax professional before making any tax decisions.

How is my retirement income taxed?

Let’s get started by talking about the common income sources that most PSERS members have in retirement and how they are taxed. Then we’ll dive into our tax strategy.

Generally, the majority of your retirement income is likely to be made up of PSERS pension payments, Social Security, and withdraws from retirement accounts like 403(b)s and IRAs. Some people may have other income from a business, rental properties and other investments, but these are less common.

PSERS Pension

Your PSERS payments are fully taxable at your federal income tax bracket. When you apply for retirement, you will elect how much tax to have withheld from each pension payment.

Social Security

Up to 85% of your Social Security is taxable. The amount that is taxable depends on your tax filing status and your income that year. This can change year to year if you experience significant changes in your income.

Pre-Tax Retirement Accounts

Withdraws you make from your 403(b), 401(k) and pre-tax IRAs are taxable. The money that you contributed to these accounts was excluded from your taxable income at the time. This means that you must pay tax when the money comes back out.

Since each of these income sources is taxable, we can assume that when you have started all of them, you will be paying more taxes, maybe the most taxes you will pay in retirement. Depending on how much income you receive from each you might even move up to a higher tax bracket.

Timing your income is key to the strategy

The tax strategy that we’re describing below is dependent on starting PSERS, Social Security and retirement account withdraws at different times. The overall goal is to create lower income years early in retirement which can be used to pay taxes at lower rates.

Let’s talk about the general timeframe for starting PSERS, Social Security and retirement account withdraws since the timing is so important to making this work.

PSERS Pension

Generally, PSERS payments start right after you retire. There usually isn’t much incentive to wait so most retirees start their PSERS payments right away. Your PSERS income will be higher of lower depending on which option you choose. Learn more about the Maximum Single Life Annuity, Option 1 and Options 2 and 3.

Social Security

Social Security payments can start as early as age 62. Waiting to start until your Full Retirement Age (FRA) provides a higher Social Security benefit. For soon-to-be PSERS retirees, The FRA is likely between age 66 and 67. You can find your FRA on your Social Security statement or by logging into your My Social Security account here. You may also delay taking Social Security up to age 70 in exchange for an even higher benefit.

To simplify all of this, just remember that age 62 is the earliest starting point and age 70 is the latest. The important thing for you to remember is that you have flexibility with when you start Social Security and that is an important part of the tax strategy.

Pre-Tax Retirement Accounts

Withdraws from your pre-tax IRAs and other retirement accounts can start as early as age 60 and are mostly at your discretion. You can make withdraws as needed to supplement your income. Once you turn 72, the IRS says that you need to take a minimum amount out of these accounts every year, whether you need the money or not. Basically, the IRS is ready for you to start paying tax on that money.

What are the basic steps of the tax strategy?

Now that we have a little basic knowledge, let’s get into the strategy. We will start with a general overview and then use a simple example and illustrations to show you how it works.

The main idea is to do your best to keep your taxable income low during the early years of retirement. What this means is choosing to delay Social Security to push that extra taxable income out into the future. For example, this might mean starting Social Security at age 68 instead of 64.

The next step is to use those lower income years before Social Security starts to either spend down some of your retirement accounts or make conversions to Roth IRAs from those accounts. This can help to lower the mandatory retirement account withdraws at age 72 when you would have PSERS, Social Security and retirement account withdraws all happening at once.

A visual example of the retirement tax problem

A visual example helps make this easier to understand so let’s take a look at a simple illustration. This is just a hypothetical and simplified example to help you understand the concept.

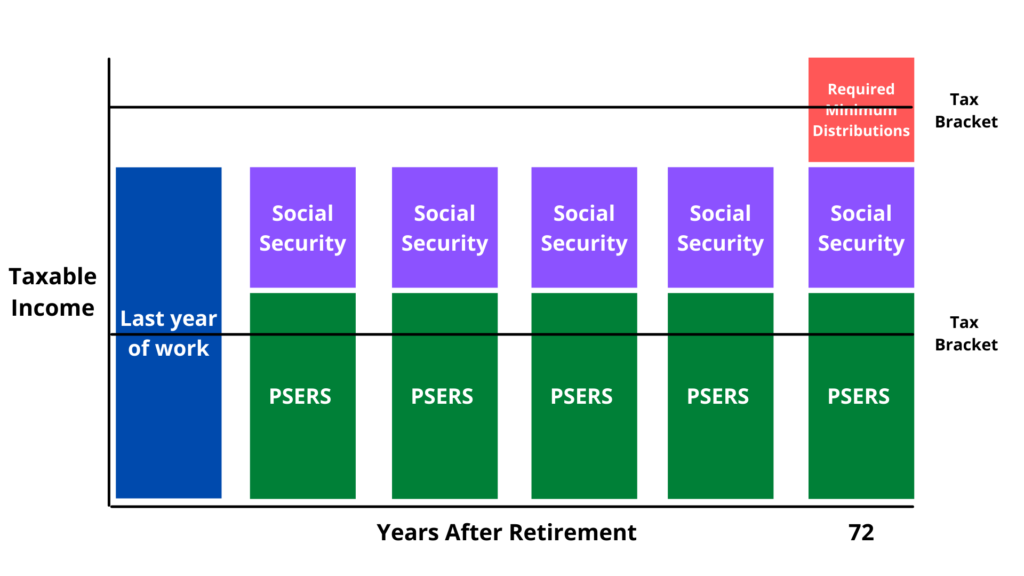

The colored columns represent the amount of retirement income in each year. The colors represent the common retirement incomes for PSERS retirees: PSERS in green, Social Security in purple and Required Minimum Distributions from pre-tax retirement accounts in red starting at age 72. The blue column represents the amount of income in the last year of work. The horizontal black lines show where hypothetical tax brackets begin.

This image illustrates a typical retirement where Social Security starts right away. You may notice PSERS alone places the retiree in the second tax bracket. A higher tax bracket is reached at age 72, Required Minimum Distributions begin. If you and your spouse have a substantial amount in pre-tax retirement accounts, your RMD could be enough to bump you up another tax bracket. If that is the case, your taxes will likely only increase as you move through retirement. This is what the strategy is meant to help avoid.

How can I avoid a higher tax bracket in retirement?

Let’s talk about a way that could help you stay out of those higher tax brackets later in retirement.

If RMDs at age 72 will cause higher taxes for you, the goal is to pay tax on that pre-tax retirement account money while you are in a lower tax bracket. The best time to do this is during the years immediately after you retire. Some people may already be in a lower tax bracket early in retirement.

Others may need to defer taking Social Security for those early retirement years to keep their taxable income lower. This helps to make room in the lower tax bracket for money you will withdraw from your pre-tax retirement accounts. This way, you can pay tax on some of your pre-tax retirement money each year before starting Social Security and potentially being in a higher bracket.

This is the very basics of the strategy- wait on Social Security to keep taxes low and use that time to pay tax on a portion of your retirement accounts each year.

How do I pay tax on portions of my retirement accounts each year?

There are two ways to pay tax on small portions of your retirement accounts early in retirement. It is important to know the difference so you can decide which, if either, is best for you.

Make a withdraw

One way is to simply make a withdraw, have tax withheld and spend the money. This might be best for you if PSERS isn’t quite enough to cover your expenses. You can use some of your retirement accounts, as needed. The amount you withdraw simply becomes taxable income for that year.

Convert to a Roth IRA

The preferred method is to make Roth IRA conversions rather than withdraws. A Roth IRA, if all of the rules are followed, allows your money to grow tax-free and be used in the future tax-free. For example, let’s say you take $25,000 from your IRA and convert it to a Roth IRA. Over the years, it grows to $40,000. You can withdraw all your original investment and the growth without paying income tax.

A Roth Conversion is completed by selecting an amount that you want to take from your pre-tax retirement account. You then move that money to a Roth IRA and pay income tax on it that year. Aside from tax-free growth, another major benefit is the IRS does not force you to take Required Minimum Distributions from Roth IRAs. You can learn more about Roth IRAs and Roth Conversions here.

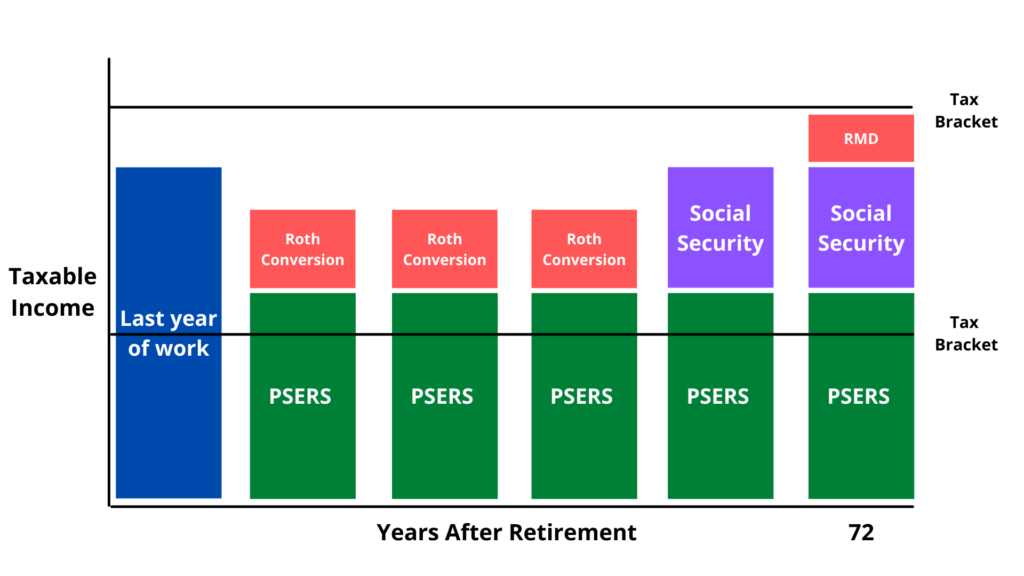

The Roth Conversion concept is shown in this illustration. Each year, you choose an amount to convert from your pre-tax accounts to a Roth IRA. You pay tax on the amount converted while in the lower tax bracket. When Social Security starts, these conversions usually stop because your income is now higher. The RMDs at age 72 should now be lower because you have taken money out of those accounts over the years already. This could help you avoid a higher tax bracket down the road and it help you build a Roth IRA where your money is growing tax-free.

Is this strategy right for me?

You might be thinking, how do I know if this strategy is right for me? Is it something that I should be thinking about?

The best place to start is by asking yourself if your PSERS benefit and other retirement income is enough to live on while you wait on Social Security. If delaying Social Security is going to put you in a financial bind, this strategy might not make sense for you.

This strategy might work for you if you have a significant amount of money in your IRAs, 403(b), 401(k) and other pre-tax retirement accounts. Your RMDs will be larger the more money you have in these accounts. Remember, for this strategy to make sense, your future RMDs must be big enough to cause a tax issue at age 72.

The Roth Conversion strategy works best if you can pay the income tax owed on the Roth conversions with cash rather than withholding the taxes from the converted amount. This way, you end up with more money growing tax-free in your Roth IRA.

For example, assume you are converting $25,000 to a Roth and you owe $5,000 in tax on that conversion. It is best to pay the $5,000 from cash so the full $25,000 will go to your Roth IRA. Alternatively, you could have the tax withheld from the $25,000 but that means only $20,000 will end up in your Roth IRA. The best result is to have as much money in your Roth IRA as possible.

Finally, this strategy only makes sense if your taxable income and tax bracket will go up later in retirement. If you are going to be in the same bracket for most or all of retirement, there probably isn’t a good reason to shift your income around to pay less tax.

So that is the strategy- defer Social Security and pay tax on your retirement accounts early in retirement while your tax bracket is lower. The best way to do this is by converting your pre-tax accounts to a Roth IRA so you get the benefit of tax-free growth. This is a simple concept with a lot of moving pieces but something all future PSERS retirees should be considering as retirement approaches.